")

The franchise sector has evolved into one of the most dynamic segments of the small business economy. Once viewed as a traditional route into food service or retail ownership, franchising has expanded into healthcare, home services, fitness, education, logistics, and professional services.

Today’s franchise businesses are more systemized, data-driven, and scalable than ever. Strong brand recognition, proven operating models, and centralized support structures have made franchising a preferred asset class for both lenders and investors.

With thousands of franchise locations generating consistent cash flow across the U.S., capital has naturally followed. Banks, SBA lenders, and private investors are increasingly active in franchise financing.

However, despite the relative stability of franchise systems, financing remains nuanced. Each deal depends on brand strength, operator experience, unit economics, and structure. For franchisees and multi-unit operators, success is not just about securing funding—it’s about structuring capital intelligently to support long-term growth.

Why Franchising Has Become a Financing Priority

From a lender’s perspective, franchises offer several key advantages.

First, franchises operate under proven business models. Unlike independent startups, franchise units benefit from standardized operations, training systems, and brand recognition, which significantly reduces risk.

Second, many franchises generate predictable cash flow supported by recurring customer demand, memberships, subscriptions, or repeat service needs. This consistency strengthens underwriting confidence.

Third, franchise brands often have established track records across multiple locations, allowing lenders to benchmark performance with greater accuracy.

Finally, franchise businesses are typically backed by strong collateral structures, including equipment, leasehold improvements, and in some cases, real estate.

Despite these strengths, lenders still apply strict underwriting standards based on operator capability and unit-level performance.

The Capital Stack: How Franchise Deals Are Structured

Most franchise financings are not funded through a single source. Instead, they rely on a layered capital stack designed to balance risk, liquidity, and scalability.

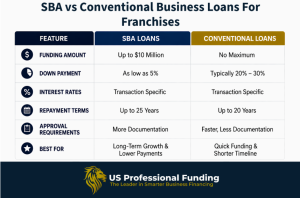

1. SBA Loans: The Foundation of Franchise Financing

SBA loans are the most commonly used financing tool in franchising, particularly the SBA 7(a) program.

SBA 7(a) loans can be used for:

- Franchise acquisitions

- Start-up costs

- Equipment purchases

- Working capital

Loan amounts can reach up to $5 million, depending on qualifications.

Key benefits include:

- Low down payments (typically 10–15%)

- Long repayment terms (up to 10–25 years depending on use)

- Competitive interest rates

Because many franchise systems are SBA-approved, this financing route is often the primary entry point for new franchise owners.

2. Conventional Bank Financing

Traditional bank loans remain an important option for strong franchise operators, especially multi-unit owners and established brands.

Banks typically provide:

- Term loans for acquisitions or expansions

- Revolving lines of credit

- Refinancing options

However, banks tend to require:

- Strong personal credit profiles

- Proven management or franchise experience

- Solid historical cash flow (for existing units)

- Lower leverage tolerance

Relationship banking is especially important in franchising, and experienced operators often work with multiple banks to optimize terms.

3. Equipment Financing: Supporting Franchise Operations

Many franchise systems rely heavily on equipment depending on the industry—whether it’s fitness machines, restaurant kitchens, medical devices, or service vehicles.

Equipment financing typically covers:

- Fitness and wellness equipment

- Restaurant and food service systems

- Cleaning or service vehicles

- Technology and POS systems

There are two primary structures:

Integrated Financing

Equipment is included within SBA or bank loans, simplifying payments and consolidating debt.

Standalone Equipment Financing or Leasing

Separate financing tied directly to equipment, often aligned with its useful life.

Each structure has trade-offs between cash flow efficiency and long-term cost.

4. Working Capital Lines of Credit

Franchise businesses often require ongoing liquidity to manage operations effectively.

Working capital needs are driven by:

- Payroll cycles

- Marketing and royalty fees

- Inventory purchases

- Seasonal fluctuations

Asset-based or unsecured lines of credit help franchisees maintain operational stability and absorb short-term cash flow gaps.

For many franchise operators, liquidity management is just as important as acquisition financing.

5. Equity and Investor Capital

Equity plays a key role in larger franchise platforms and multi-unit expansion strategies.

It is commonly used for:

- Multi-unit acquisitions

- Regional development deals

- Fast growth rollouts

- Brand scaling strategies

While equity reduces leverage and strengthens balance sheets, it also introduces ownership dilution. However, strategic equity partnerships can accelerate expansion far beyond what debt alone allows.

6. Seller Financing and Hybrid Structures

Seller financing is frequently used in franchise resales and multi-unit transfers.

Benefits include:

- Reduced upfront capital requirements

- Easier deal structuring

- Alignment between buyer and seller

Most franchise acquisitions involve a combination of SBA debt, seller financing, and buyer equity to bridge valuation gaps and reduce lender risk.

What Lenders Actually Look For

Even though franchising is considered lower risk than many independent businesses, lenders still conduct detailed underwriting.

1. Cash Flow and Debt Service Coverage

The primary question remains:

Can the franchise support its debt obligations?

Key metrics include:

- EBITDA stability

- Net margins by unit

- Royalty and fee structure impact

- Operating expense control

Lenders often normalize earnings to reflect true cash flow performance.

2. Franchise Brand Strength and Unit Economics

Not all franchise systems are equal.

Lenders evaluate:

- Brand reputation and national footprint

- Franchise disclosure document (FDD) performance trends

- Average unit volume (AUV)

- Franchisee success rates

Stronger brands significantly improve financing approval odds.

3. Operator Experience and Management Capability

In franchising, the operator matters as much as the brand.

Lenders look for:

- Prior franchise or industry experience

- Multi-unit management capability

- Operational discipline

- Financial literacy

Even strong brands can be declined if the operator lacks experience.

4. Location Performance and Market Dynamics

For unit-level financing, location is critical.

Lenders assess:

- Foot traffic or service demand

- Market competition

- Demographic alignment

- Lease structure and terms

Strong locations improve both cash flow and collateral quality.

5. Franchise System Support and Stability

Franchise systems that provide strong operational support reduce lender risk.

This includes:

- Training programs

- Marketing support

- Supply chain systems

- Operational oversight

Stable franchisors improve overall credit confidence.

Financing Different Types of Franchise Projects

Franchise Acquisitions

Acquisitions are the most financeable franchise transactions due to existing cash flow.

Typical structures include:

- SBA 7(a) loans

- Seller financing

- Buyer equity

- Bank term loans

New Franchise Startups

Startups are higher risk and require stronger operator profiles.

Financing often includes:

- SBA loans

- Personal equity injection

- Equipment financing

- Working capital reserves

Multi-Unit Expansion

Growth-focused franchisees often pursue multi-unit development.

These deals may include:

- Portfolio-level SBA financing

- Private equity partnerships

- Strategic debt facilities

Franchise Real Estate Development

Some franchise models require ground-up development or buildouts.

Typical financing stack:

- SBA 504 loans

- Construction loans

- Equipment financing

- Equity investment

Common Financing Mistakes to Avoid

Underestimating working capital needs

Many franchisees underestimate cash requirements during ramp-up periods.

Overleveraging early units

Excess debt can limit expansion opportunities.

Ignoring franchise system performance data

Not all franchise brands perform equally across markets.

Misaligned financing structures

Using short-term debt for long-term assets can strain operations.

Failing to shop lenders

Franchise financing terms vary widely between institutions.

The Future of Franchise Financing

Several trends are shaping the future of capital in franchising:

- Continued growth of multi-unit operators

- Expansion of service-based franchise systems

- Increased private equity involvement

- More data-driven underwriting models

- Greater SBA participation in franchise lending

As franchising continues to professionalize, financing structures are becoming more sophisticated and competitive.

Final Thoughts

Financing a franchise business is not just about securing capital—it’s about structuring it strategically.

The most successful franchise operators understand that:

- Brand strength directly impacts financing options

- Cash flow discipline determines scalability

- Proper capital structure drives long-term growth

When executed correctly, financing becomes a strategic advantage—allowing franchise owners to expand faster, operate more efficiently, and build multi-unit enterprise value.

Author

Christopher Cornella is the Vice President of Business Development at US Professional Funding, where he specializes in providing tailored financing solutions for franchise owners, developers, and investors nationwide. With extensive experience in financing, acquisitions, expansions, equipment, refinancing of existing debt, and ground-up construction start-ups, Chris works closely with operators across the franchise industry to help them scale efficiently and maximize profitability. Chris can be reached at: [email protected], 848-231-8464, https://usprofessionalfunding.com/industries/franchises/, https://usprofessionalfunding.com/ and https://usmedicalfunding.com.